![]()

Midyear Market Update

Hello all – I thought I would check-in and share an update now that we are a little over halfway through 2017.

Here is some raw data taken from our friends at the Sherman Sheet:

In the markets:

In the U.S. markets last week, it was the Dow…and then everyone else. The Dow Jones Industrial Average rose over 250 points last week closing at 21,830. The tech-heavy Nasdaq Composite fell 13 points to close at 6,374 points, a decline of -0.2%. The large caps fared better than their smaller brethren.

In U.S. economic news, the number of Americans who applied for initial unemployment benefits increased slightly last week, but remained near its lowest level in decades. The Labor Department reported initial jobless claims for the week ending July 22nd increased by 10,000 to 244,000. The less-volatile four-week moving average of claims remained unchanged at 244,000. New claims have remained under the key 300,000 threshold that analysts use to indicate a healthy jobs market for 125 straight weeks – its longest run since the early 1970’s. The number of people who have already been receiving unemployment benefits, so-called continuing claims, fell by 13,000 to 1.96 million. Continuing claims have been under the 2 million level for 16 straight weeks – event not seen since 1973.

I mentioned in a recent email and to many of you in reviews over the past quarter that we are following the homebuilders space very closely so far this year. Below is some detailed information from the Sherman report on the U.S. housing market. I believe the numbers can really help to articulate our view of the space.

Sales of previously-owned homes fell to the slowest pace since February as limited supplies of homes for sale continue to weigh on the housing market. Existing home sales were at a seasonally-adjusted annualized rate of 5.52 million homes last month, according to the National Association of Realtors (NAR). The reading was 0.7% higher than the same time last year, but a 1.8% decline from May’s reading. In addition, it was the second lowest reading of the year. Supply continues to be the biggest factor affecting the existing home sale market, says NAR. Total inventory was down 7.1% from the same time a year ago, and at the current sales rate there is only a 4.3 month supply of homes on the market. Zillow’s Chief Economist Svenja Gudell said, “It’s difficult to sell homes when there are so few available to buy, and the chronic inventory shortage the market has been suffering from – bordering on an inventory crisis at this point – is now more than two years old.” The supply imbalance continues to push prices higher. The median sales price was $263,800, a 6.5% increase compared with the same time last year. That sets a fresh record and marks the 64th consecutive month of yearly price gains. Of concern to economists, housing prices are growing at roughly double the pace of wage gains and thus the rate of price growth is unsustainable.

New home sales increased for a second straight month, according to the Commerce Department. New home sales for June were at a seasonally-adjusted annual rate of 610,000, an increase of 0.8% from May. June’s reading was 9.1% higher than a year ago. The median sales price of a new home was $310,800 in June, a 3.3% decline compared to the same time last year. At the current sales pace there is a 5 month supply of homes on the market. Stephen Stanley, chief economist for Amherst Pierpont Securities said in a research note, “I am not worried about flagging demand, as builders and realtors have been very clear that the demand is there.”

U.S. Gross Domestic Product (GDP) grew at a 2.6% annual rate in the second quarter, according to the latest data from the Bureau of Economic Analysis. Consumer spending, the main driver of the U.S. economy, led the increase with a 2.8% gain, while business investment in equipment rose 8.2%.

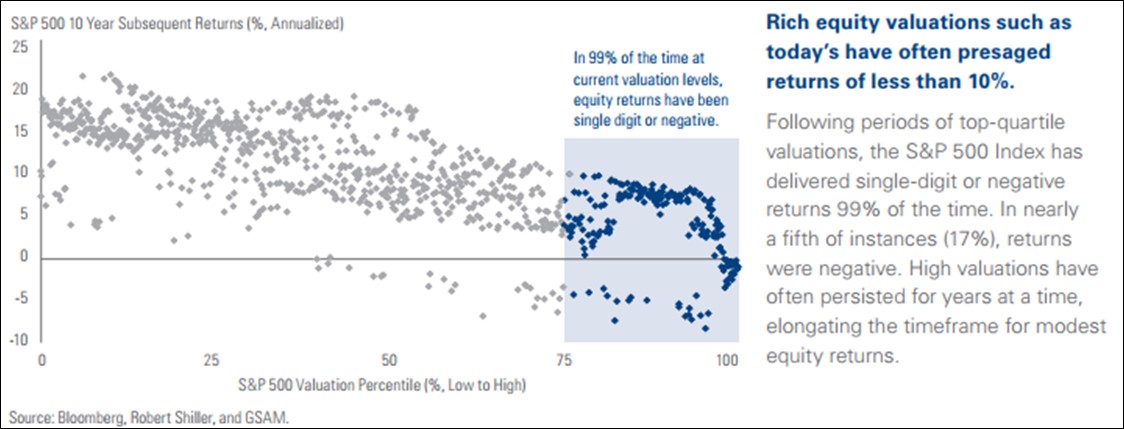

Also from our friends at the Sherman Sheet, some fairly sobering statistics on investment returns after investing in a market at our current level: in layman’s terms – 99% of the 10 year periods after a market valuation like we see today, returns were either single digit or negative.

Here are the details to back that statement from Goldman Sachs: “recently released research that reveals a different take on the relationship between present stock market valuations and future returns. Goldman reports that after periods of valuations in the top quartile of all historical valuations, the S&P 500 index has delivered single-digit or negative returns 99% of the time. In nearly a fifth of instances (17%), returns were negative. Unfortunately, current stock market valuations are solidly in that upper quartile.”

(sources: all index return data from Yahoo Finance; Reuters, Barron’s, Wall St Journal, Bloomberg.com, ft.com, guggenheimpartners.com, zerohedge.com, ritholtz.com, markit.com, financialpost.com, Eurostat, Statistics Canada, Yahoo! Finance, stocksandnews.com, marketwatch.com, wantchinatimes.com, BBC, 361capital.com, pensionpartners.com, cnbc.com, FactSet; Figs 1-5 source W E Sherman & Co, LLC)

I do not include that last fact on valuations to scare anyone away from continuing to invest. I only point it out to further enforce the fact that we are at a very interesting point in investing history, very similar in many ways to 2007. Hi valuations, high real estate prices, low unemployment, a Federal Reserve struggling to raise interest rates… All of these factors would suggest we take a close look at both: actively managing risk in your portfolio (which is what I do on a daily basis), and considering some safe harbor money that could provide steady income for you in retirement (locking in the gains we have made over the past several years).

If it is time for a tune up, you have other assets outside ASG that are not being actively managed, or you are interested in income creation options that we can employ, please call or email for a time to meet.